Navigating investment choices? 9 areas to explore.

Written: 26 August 2022

Author: Kirsty O'Hara

8 min read

The million-dollar question is often: how do I choose a good investment?

If you don’t have an uncle or family member that works in finance, it’s tempting to think fees are the only metric to consider when selecting investments. While fees are an important consideration, there are other important factors to consider before you click ‘buy’ on a fund.

No different to selecting a university, or a suburb to live, investing also requires its fair share of due diligence. You almost want to ‘date’ a fund manager before you buy a fund. You want to get an idea for who the people are, what philosophy they follow, and if you agree with the integrity of the company. For many investors you are going to hold this investment over years, or even decades, so you want to be sure that the investment provider is a good fit with your personal values and financial goals. Like any relationship, you want to know you can ride the realities of life together.

The Financial Markets Authority (FMA) encourage that we focus on understanding risks, returns and costs when selecting investments. As the regulators of financial services based in New Zealand, the FMA also point out that it is illegal in New Zealand to sell an investment through an unsolicited communication, such as a cold call. So do be wary of any unsolicited communications. They also urge you to be wary of any investment that sounds too good to be true, and suggest that investors avoid ‘get rich quick’ schemes.

The FMA champion the idea that you can start investing with small amounts; and suggest KiwiSaver, Managed Funds, and ETF’s can be a great place to start when considering investments. They emphasise that investors should carefully review each fund’s product disclosure statement (PDS), annual report and quarterly update prior to investing. For ease of reference you can find the PDS and RIPPL Effect reports (which we explain in another article here) within the Flint app. These two documents between them, should have a lot of the information you are looking for during the following detective hunt. Sorted’s Smart Investor and Mindful Money are two other great websites worth bookmarking as research side-kicks.

Warren Buffet is famous for saying “if you aren’t willing to own a stock {or investment} for ten years, don’t even think about owning it for ten minutes.”

This is sage commentary, which you could flip the other way to consider: if you’re planning to own an investment for ten years, why not spend some time researching it amongst other investment offerings. When playing the long game, you can probably appreciate that time invested early on into researching and selecting investments will build the foundation of your investment strategy – so we give you permission to take some time to understand the investments you are considering across the following areas:

1. Corporate and Investment Governance

First up, it’s good to understand the backbone of your investment and the company who will be working on your behalf to grow your wealth. Some good questions to ask include:

- When was the fund manager founded?

- How are the board and key leadership teams structured?

- What experience do the key investment personnel have?

- If considering international investment providers - has the investment provider, or any of the core management team, previously filed for bankruptcy?

- Is the fund manager locally owned?

2. Investment Philosophy and Process

Every fund manager will have a philosophy they apply to their investment process. To understand how they make investing decisions, you may like to explore:

- What investments does the fund make?

- What are key frameworks that support the buying and selling decisions of the fund?

- Does this fund, or fund manager utilise an active or passive, growth or value, approach when selecting companies to invest in?

If you are considering a fund that believes in sustainable, impact or ESG investing – then you also may like to consider:

3. ESG & Sustainability Framework

When considering Environmental Social Governance (ESG) investments, there are a variety of frameworks for consideration.

Some investment providers champion the thinking that we can:

Invest in the good: Invest in companies with better environmental and social scores. Environmental considerations include issues that affect nature, such as waste and pollution, resource depletion, deforestation, and climate change. Social considerations include issues that affect people, such as working conditions, human rights issues, and community impacts.

Engagement and influence: Engage with companies by using shareholder voting rights and seat at the table to take a proactive role in encouraging companies to act responsibly.

Impact investment: The intention to generate a positive, measurable, social and environmental impact alongside a financial return.

Other fund managers make decisions based on an exclusions framework (where they avoid specific companies, and operate from a ‘do no harm’ ethos).

Many funds these days will boast a Responsible Investment Association of Australasia (RIAA) badge; which confirms the fund meets a certain set of responsible investing criteria. This certification appeals to many investors, who find it reassuring to know the fund has a responsible certification. We talk more about RIAA here.

No matter your stance on ESG investing, you will want to understand the guiding principles of the investment you are considering. You may like to consult the Sorted Smart Investor or Mindful Money, to better understand the holdings and composition of a fund. Mindful Money also offer badges, for funds that exclude specific areas of concern for investors. Eg. Weapons or Fossil Fuels. Their exclusion graphics can also be a helpful reference.

It’s worth noting that many socially responsible investments hold equities (shares), and as a result may be seen to be more suited to investors with longer time horizons. If you have a short time horizon (less than 10 years) then definitely do your research wisely to ensure you can achieve your financial goals while maintaining alignment with your personal values.

4. People & Leadership

It’s easy to be mistaken that investments are about numbers, when they are also just as much about people behind the numbers. The team of specialists managing an investment can be pivotal to the success of a fund. Some helpful questions to ponder when considering people and leadership include:

- How is the fund being managed?

- Who is accountable for managing the fund?

- Do the staff and fund manager invest in their own funds? If they do, it supports the theory that they have skin in the game to want the investment selections to do well. Are they paying the same fees as other investors?

- Is the investment team’s work history relevant to the specific funds that they manage?

- Have there been changes to the fund – its strategy or key people?

- Does the fund manager have a high turnover of staff?

5. Portfolio Construction and Implementation

If you thought of a managed fund like a cake, you’d want to know what flavour you were considering. Carrot, banana, chocolate? All could be good options, but made from slightly different ingredients with a slightly different end result.

Here’s some questions to understand the key ‘ingredients’ of an investment your considering:

- Geographically, which areas is the fund invested in?

- Which asset classes does the fund invest in? eg. equities (shares), property, infrastructure, bonds or cash?

- Is the investment you are considering a single or multi-asset fund?

- What is the liquidity of the fund? (Liquidity helps us to consider how easily an asset or security could be converted into ready cash without affecting its market price. We've included a short summary of ways to consider liquidity below).

- How much of the fund is held in cash? And what is the rationale for this?

- Does the fund have a ‘buy and hold’ mentality? Or do they have a team of specialists actively looking for opportunity and trading accordingly, in the hopes of outperforming the market?

- Does the fund have a growth or value or income strategy?

- Is there an industry benchmark that the investment provider is aiming to beat?

- What are the key drivers of the fund’s performance?

Liquidity Measures:

Measurements to address liquidity risk can vary. They may take into consideration the particular characteristics of a fund, to include:

- the fund's investment objectives and investment strategy;

- the fund's dealing frequency;

- the fund's investor base; the nature of the assets under management;

- and the fund's liquidity needs under a range of market conditions.

6. Risk Management

With any investment it’s imperative to ask what are the risks of investing in this Fund?

To identify risk, be sure to consider:

- Is it likely the fund you are considering will out-perform inflation?

- Will the fund you are considering be impacted by any market volatility? For example, aggressive or growth funds with a high composition of shares may carry more risk.

- Is the fund concentrated? i.e. have a limited numbers of holdings and hence have less diversification. If you’re considering a managed fund, what does the manager say about how they manage risks?

- How might this fund respond in certain market climates? Have they navigated uncertain times successfully before?

- Is the fund reliant on a particular person?

You'll also want to consider the risk rating of the fund? The PDS and RIPPL Effect reports will always include a risk indicator. A risk rating of 1 is a low risk fund, and a risk rating of 7 is extremely high risk. Keep an eye out for these graphics when reading PDS and RIPPL Effect reports:

7. Fees : Will they stop your money growing?

Understanding fees is a hurdle worth conquering. The FMA point out that: “Lower costs mean more of your money stays invested, and the power of compounding returns means these savings will contribute significantly to your long-term returns”.

Here’s some great questions to start getting your head around fees:

- How are fees charged? The product disclosure statement (PDS) for each fund manager will explain this.

- What fees and charges do you pay? Management fees? Administration fees? PDS documents refer to the ‘estimated fee’ for the fund which is the fee your are projected to pay in the coming year.

- For a managed fund, what fees has the fund charged in the past year? You’ll see below we talk a bit about Total Expense Ratios (TER) which relate to this.

- Does the fund manager charge a performance fee? And if so, how is this structured to ensure it is motivating for both investors and managers? What does the fund manager have to do to receive the performance fee?

- Are there Buy/Sell or Entry/Exit fee’s charged?

Within Flint itself you will see a ‘management fee’ and a TER.

The management fee excludes gst, and is the base fee charged by the fund manager.

On Flint the TER is explained as:

The Total Expense Ratio (TER) includes the management fee, other administration fees and any actual performance fee for the last year quoted by the manager in its latest disclosure. The TER doesn’t include any transaction costs incurred by the fund. If we don't display a TER, the fund may be too new to display any past fees. More details, including estimated future fees, can be found in the fund’s product disclosure statement.

When considering some fund managers - like SuperLife - you will notice there is not a lot of difference between the management fee and the TER, because the only difference here is that the TER includes gst.

For other fund managers, such as Fisher Funds, you will notice that if they have had a particularly good investment period recently then their TER will likely be a lot higher than the management fee - due to the inclusion of relevant performance fees.

Many people have different opinions on whether performance fees are worthwhile. Some believe that a fund manager can be more motivated to achieve returns, if rewarded with a performance fee. Other people debate if passive investments or active investments are more worthwhile over the long term - which we explain over in our Active vs Passive article here.

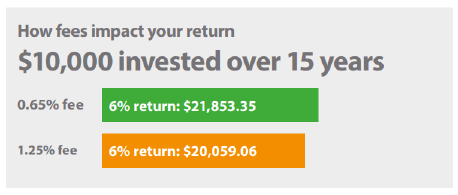

This FMA example highlights the potential impact fee’s may have:

The FMA also comment: “Only pay higher fees if you’re confident you’ll be persistently rewarded with returns high enough to make it more financially worthwhile than an investment with lower fees. For example, if you were confident that by paying the higher 1.25% fee, you’d make a 7% return on your $10,000 investment, it would be worthwhile. This is because your return after fees would be higher than if you’d paid lower fees and achieved a 6% return.”

Please strive to understand fees. While they are not the only metric to consider they can have a huge impact on your investment balance over time.

It’s worth remembering: Fees are usually shown in percentages. Small percentage differences can mask how much impact fees have in actual dollar terms.

8. Managed Fund vs ETF

ETFs (Exchange Traded Funds) usually track a market index which is known as a passive investment (providing a market return). They have a simpler fund management strategy, so fees on ETFs are usually cheaper. ETFs are also more likely to be single asset funds, while managed funds offer a broader range of multi-asset funds. ETFs therefore tend to requires a bit more knowledge, to ensure you build a diversified investment portfolio.

If you are weighing up between managed funds and ETF’s the FMA kindly composed this handy chart, which shows the key differences between a Managed Fund and an ETF:

You will also have to pay brokerage when you buy or sell an ETF.

The other thing to acknowledge when comparing managed funds and ETF’s is acknowledge that they are taxed differently:

9. Tax & Trading Implications

We won’t deep dive into tax implications of investments here, however if you are weighing up between investing in managed funds and ETF’s then tax differences are worth understanding.

Money Hub sum up the difference between the two by saying:

“Tax - New Zealand ETFs are classed as listed PIEs, which means the tax rate is fixed at 28%. If you pay a lower tax rate, you'll have to claim the overpaid tax from the IRD on your tax return at the end of the financial year. This will appear as a credit to offset any other personal tax. If you are investing for a child or charity, where there is no other taxable income to offset the tax credits against, you may be overtaxed using an ETF. If you've invested in an overseas ETF, i.e. via Hatch, Stake or Sharesies, you will pay specific US tax as well as NZ tax (via an IR3 form). Index funds are different - tax is deducted at the correct rate and paid directly to the IRD. Unlike ETFs, index funds don't have a tax effect which sees a portion of your investment sitting idle until tax return time.”

It's also essential to consider trading costs, when looking at tax implications. When buying and selling ETFs you may want to factor in brokerage fee’s. Index funds by comparison avoid brokerage, price spreads or registry fees.

Getting clear on what these costs and tax implications are, helps to make sure you are not swayed by a false economy. On the whole, managed funds keep tax implications very simple for investors. If you’re time poor, but investment rich, a managed fund can be worth consideration due to the lower admin requirements for the investor.

Conclusion:

At Flint we are the first to admit that the language of investing can be difficult to wrap your head around, the sheer number of options can be overwhelming, and the rules of what to do when can seem confusing. We hope the above factors make navigating the investment landscape a more streamlined process.

In addition to exploring the above nine areas, it goes without saying that you will likely want to consider the performance metrics of the fund. When reading the digital tear sheets, PDS, and other research documents - do keep in mind the objectives of the fund manager - and how the fund performance is likely to measure up against these performance forecasts. If they plan to outperform a benchmark, make a call as to if you think they will realistically achieve that performance goal. While many people consider the past performance of a fund (or fund manager) it's always important to note that past performance does not guarantee future returns.

If you would like additional information on getting started, these two guides put together by the FMA are well worth a read:

- Wise up and Invest Well: Guide to investing in Managed Funds and ETF’s (available here)

- Hits and Myths – An introductory guide to investing (available here)

And if you’re just getting your head around how the tools and insights on Flint can help, then the following articles may be worth a browse too:

Happy investing!

Flint

IMPORTANT NOTICE AND DISCLAIMER:

All content shared is of a general nature, current to the time it was penned, and is not financial advice. Before making any investment decisions, please be sure you have completed full due diligence. This should include reading the product disclosure statement (PDS), considering fees and taxation, identifying your time horizons, and understanding the performance history and reputation of the investments you are considering.

Please note: When investing you are not guaranteed to make money (and on occasion you may lose some or all of the money you began with). Seek independent advice to establish if an investment is suitable for your financial situation and long-term wealth generation goals.

Sources:

https://sorted.org.nz/guides/saving-and-investing/about-investing/

https://www.fma.govt.nz/consumer/investing/types-of-investments/managed-funds/

https://www.fma.govt.nz/consumer/investing/deciding-how-to-invest/

https://www.fma.govt.nz/library/investor-resources/topinvestingdosanddonts/

https://www.fma.govt.nz/assets/Consumer-section/HitsandMyths-MaryHolm-Guidebook.pdf

https://www.fma.govt.nz/consumer/investing/investing-basics/

https://www.fma.govt.nz/assets/Consumer-section/20190926-Managed-Fund-Guide.pdf

https://www.fma.govt.nz/consumer/investing/types-of-investments/exchange-traded-funds/

https://www.fma.govt.nz/assets/Guidance/MIS-liquidity-risk-management-guide.pdf

https://www.moneyhub.co.nz/index-funds-vs-etf.html

https://www.investopedia.com/terms/l/liquidity.asp